Fees and Expenses on Mutual Funds and ETFs: A Complete Guide to the Often Misunderstood and Hidden Costs of Investments

Investing plays a massive role in growing and preserving your wealth over the course of your lifetime. Along with defining your investment philosophy and selecting appropriate investments, it’s essential to have an understanding of the various expenses you may come across while investing, as every expense you incur will diminish the growth on your investment earnings.

Below, we’ll explore the common fees associated with actively managed and passive funds as well as ETFs – the expenses to watch out for with each type of investment.

We’ll also discuss how your investment platform can have an impact on the costs too.

The More Commonly Known Fees Associated with Investing

Whether you are self-managing your investments through a platform like Vanguard or seeking guidance from a robo-advisor or financial advisor, it’s important to be mindful of the more common kinds of investment expenses and fees.

Below are the relatively well understood fees that that are typically associated with investing in mutual funds and ETFs.

Trading fees

When you are investing on your own, there are some additional administrative costs you’d benefit from understanding before trading your investments.

These includes expenses such as:

- Purchase fees: similar to a front-end sales charge (see A shares above), but instead it’s going to the fund rather than a commission to a broker or advisor

- Redemption fees: similar to a back-end sales charge (see B shares above), but also going directly to the fund instead of a broker or advisor to prevent excessive trading

- Exchange fees: may be imposed if exchanging your fund to another fund offered by the same fund group to also prevent excessive trading

Platform fees

When you invest with a custodian like Vanguard or Fidelity, you’ll want to be aware of any additional expenses, like transaction costs and account maintenance fees, even if minor.

Transaction costs will vary depending on where you do your investing, what you invest in, and how often securities are bought and sold. Account maintenance fees may be waived as well depending on the minimum requirements.

For example, Fidelity charges no account fee while Vanguard may charge a $20 fee for certain accounts, but this can be waived with $1,000,000 in Vanguard assets or through email delivery of statements.

It’s important to do your research when choosing a custodian as a DIY investor.

NOTE: If your primary investing is through your employer’s 401(k) plan, you’ll want to understand the fees involved through this platform as well.

Fees for Advice from Either a Robo-Advisor or Human Advisor

Probably the biggest fee anyone pays when investing in mutual funds and ETFs are advisor fees. The amount you pay will depend on the type of advisor you use, how much money you are investing, and the type of fee structure the advisor charges.

Here is a quick summary:

RoboAdvisor Fees: If you are a DIYer but also prefer some additional investment guidance, you may be utilizing a robo-advisor. A robo-advisor is an automated online platform that provides algorithm-driven investment management services with minimal human interaction.

Most robo-advisors charge lower fees than traditional financial advisors because they invest your money in pre-established portfolios made up primarily of low-cost funds. NerdWallet maintains a list of the best robo-advisors based on certain criteria.

- RoboAdvisors typically charge an Assets Under Management (AUM) fee of of 0.25% to 0.50%. (AUM means that you are paying the advisor a percentage of your savings. So, if you have $500,000 in savings, you pay $1,250 to $2,500 a year.)

Advisor Fees: Meanwhile, if you prefer a completely hands-off investment approach and work with a financial advisor to manage your money, you’ll need to account for their fees as well. For the majority of advisors managing money today, an AUM (Assets Under Management) fee is still prevalent.

- According to a 2023 report by Advisory HQ, the average financial advisor fee in 2023 was 1.02% for $1 million AUM, which adds up to $10,200 annually.

NOTE: If you work with an advisor under an AUM arrangement, you’ll want to factor in these costs when entering in your rates of returns for your investment accounts within the NewRetirement Planner.

It is also possible to work with an advisor who is fee-only, meaning they charge a pre set fee for agreed upon services. NewRetirement offers fee-only advice from a CERTIFIED FINANCIAL PLANNER professional. Services include investment guidance. Book a FREE discovery session.

professional. Services include investment guidance. Book a FREE discovery session.

Other Kinds of Investing Fees

Besides fees for advice and trading, there are a whole host of other fees that are associated with both actively managed funds and even passively managed funds and ETFs.

Explore these fees below.

The More Hidden Fees Associated with Actively Managed Funds

An actively-managed mutual fund is managed by professional fund managers who are utilizing their deep expertise and research to hand-select stocks, bonds or other holdings for the fund. They actively trade the holdings in the fund and their ultimate goal is to outperform a specific benchmark or market index.

Active managers are looking to beat the market through targeted investing, timing the market and any number of strategies that seek higher than average returns.

Pros and cons of an actively managed fund: As with any investment, there are pros and cons. Here are some of the downsides:

- There’s additional risk in that the portfolio manager may very well underperform its benchmark.

- An actively managed mutual fund could also have more taxable capital gains because the portfolio manager may trade more often.

- They generally have more fees associated with them.

Let’s explore the fees:

Expense ratios and their various components

The management and marketing of actively-managed mutual funds result in expenses and costs that are often passed on to you as the investor. These annual ongoing fees can include management fees, 12b-1 or distribution (and/or service) fees, and other administrative and operational expenses.

These fees make up the expense ratio, which represents the total percentage of a fund’s assets. In the investment world, the expense ratio is also referred to as annual fund operating expenses. Each year, the fee is automatically taken from the fund’s gross return and transferred directly to the fund manager.

It’s essential to understand the components of an expense ratio because doing so provides a clearer picture of the fees you’ll incur when investing in an actively-managed mutual fund.

Management fee: Part of the expense ratio of your investment may include a management fee, which covers the salary of a portfolio manager and their staff to buy and sell the investments within the fund.

This fee will vary depending on the size of the fund and the strategy it pursues.

12b-1 fee: If you are invested in an actively-managed mutual fund, you may be paying what’s called a 12b-1 fee. Although, not all mutual funds have 12b-1 fees.

A 12b-1 fee is essentially the fee you are charged for someone selling you a mutual fund. 12b-1 fees are considered operational expenses and are included in the overall expense ratio for the investment fund. The fee is used to cover the expense of advertising, marketing, and distribution.

A 12b-1 fee can be as high as 1% annually for a mutual fund.

Other expenses associated with managed funds: Along with the management fee and 12b-1 fee, there may be “other expenses” as part of the expense ratio. Generally, these aren’t as transparent when looking up the expense ratio for an investment you may be researching.

Other expenses may include:

- Accounting and legal expenses

- Transfer agent expenses (e.g. maintaining shareholder records and reports)

- Administrative costs

Relearning your ABCs…of sales loads on managed funds

There are many actively-managed mutual funds that are sold with a sales load. These are fees that can be charged to you either at the time of purchase or at the time of redemption (or sale) of your mutual fund.

Load funds with varying sales charges are usually differentiated by their share classes:

- A shares: A front-end sales charge, reducing the amount of money invested during the initial purchase

- B shares: A back-end (or deferred) sales charge when you sell your fund (this fee may be waived or decrease over time and converted into A shares if held for a certain number of years)

- C shares: No front-end or back-end sales charge, but generally a higher 12b-1 fee on an annual basis (i.e. a level sales charge); a small sales charge may be imposed if you sell within a year of purchase as well

Uncovering the Hidden Fees and Expenses on Passively Managed Funds and ETFs

Investments that are part of a passive management investment philosophy would include index funds and ETFs.

Where active managers are looking to beat the market, passive investors are just focused on trying to capture the returns of the market while keeping costs low.

However, there are still fees associated with these investments.

What is an index fund?

Index funds simply buy and hold the stocks (or bonds) in all or part of a specific market you are looking to capture as part of your investment. For example, by buying a share in a “total market” index fund, you acquire an ownership share in all the major businesses in the economy.

Index funds eliminate the guess-work (and increased anxiety levels) of trying to predict which individual stocks, bonds or mutual funds will beat the market. They are instead designed to keep pace with market returns.

What is an ETF?

Like mutual funds, Exchange-Traded Funds (ETFs) are investment funds made up of pools of securities. But unlike mutual funds, ETFs are bought and sold on stock market exchanges just like stocks. Since ETFs are traded on the exchange like stocks, they can be bought and sold at any time. You don’t have to wait for the market to close.

While there are some actively-managed ETFs, most are designed to track market indexes, just like index funds.

ETFs can also be more tax-efficient than mutual funds since they tend to distribute fewer (if any) capital gains.

NOTE: When you are adding your investment accounts into the NewRetirement Planner, you should be thinking about the mix of stocks, bonds and cash in each account in order to enter an appropriate rate of return assumption.

Expense ratios on index funds and ETFs

Just like with actively-managed mutual funds, you’ll want to pay attention to the expense ratio for index funds and ETFs as well. The expense ratio may look (significantly) lower than your typical actively-managed mutual fund.

In fact, according to the Investment Company Institute (ICI) 2022 report “Trends in the Expenses and Fees of Funds, 2022”, the average expense ratio for actively managed equity mutual funds was .66% in 2022 vs. the average expense ratio for index equity mutual funds of .05% and average equity ETF expense ratio of .16%.

Both index funds and passively-managed ETFs have low expense ratios due to the lack of a fund manager, often avoiding a lot of the fees making up the expense ratio of an actively-managed mutual fund, like a 12b-1 fee and other expenses.

Can you avoid a sales load? Yes, you can!

Thankfully, not all investments have sales loads.

With no-load funds, you do not pay a commission to buy or sell shares. Instead, you as the investor are doing the research and filling out the forms to purchase the fund. So, if you’re looking to purchase $20,000 worth of a no-load mutual fund, all $20,000 will be invested into the fund.

The majority of index funds, ETFs and even some actively-managed funds don’t charge a load.

How to Identify Fees on Your Active and Passive Funds and ETFs (with Examples)

If you are invested in a mutual fund or an ETF – either actively or passively managed – you will have access to your fund’s prospectus.

Along with outlining the strategy and what it is invested in, a fund’s prospectus includes a full breakdown of the fees and expenses you can expect to pay. You will generally find the prospectus by visiting the fund’s website or calling the mutual fund directly.

In addition to your investment’s prospectus, there are other resources to determine the expenses of the funds you are invested in, like Morningstar or FINRA’s Fund Analyzer.

Let’s take a look at an actively-managed mutual fund, index fund, and an ETF to gain further insight into these different types of expenses.

DISCLOSURE: These are not investment recommendations.

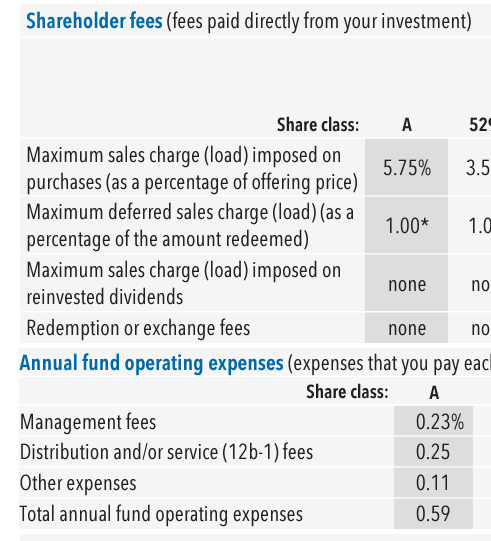

Analysis of fees on American Funds American Mutual A (AMRMX)

This is an actively-managed mutual fund from American Funds with a sales load. Below is a page from the prospectus outlining expenses of the fund for the A share class:

Given it’s an A share class, you can see there is a 5.75% maximum sales charge (load) imposed on purchases. This sales charge will vary depending on the initial amount you invest. For example, if you invest $10,000, the initial charge will be 5.75% (or $575). Meanwhile, if you invest $50,000, the initial charge will be 4.5% (or $2,250).

The total annual fund operating expenses, or expense ratio, is 0.59%, which is made up of the 0.23% management fee, 0.25% 12b-1 fee, and 0.11% in other administrative expenses. That means it only takes 0.34% to run the mutual fund (pay staff, office space & equipment, and more). The other 0.25% goes to paying for ads and marketing the mutual fund to investors.

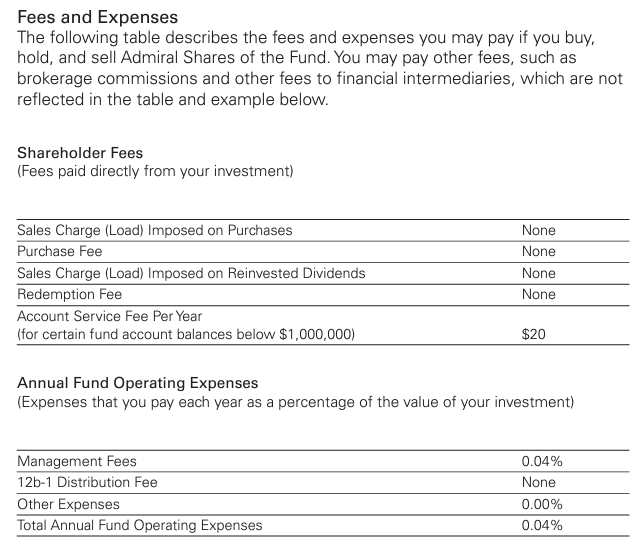

Analysis of fees on Vanguard Total Stock Market Index Admiral (VTSAX)

VTSAX is a popular index fund that is also considered a no-load fund. Below is a snapshot of expenses from its summary prospectus:

As you can see, there is no sales load and the total expense ratio is only 0.04%. The only shareholder fee consists of an account service fee of $20 per year, with specifications.

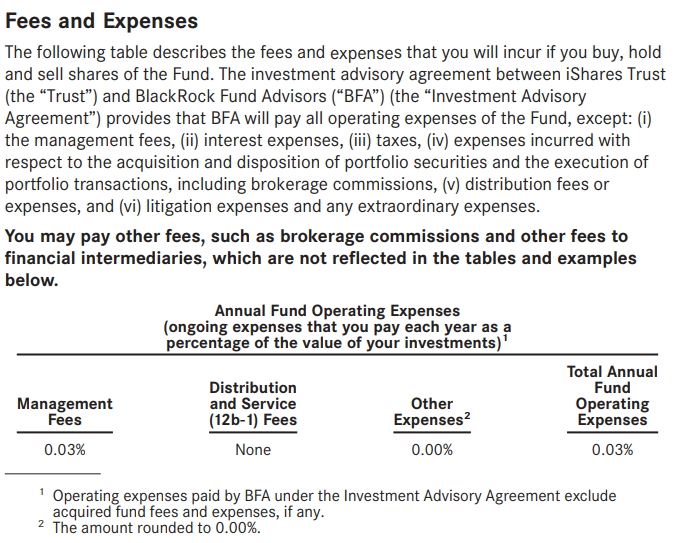

Analysis of fees on iShares Core S&P 500 ETF (IVV)

This fund represents an Exchange-Traded Fund, or ETF. The expenses page from the summary prospectus shows the following:

As you can see, this fund represents the lowest expense ratio (i.e. total annual fund operating expenses) out of the three examples, at only 0.03%.

While conducting your research on funds, be sure to review the prospectus as you can gain a lot of valuable information that will play a role in your investment decisions.

You Can’t Ignore Expenses as Part of Your Financial Plan

Expenses are one of the key drivers of the success of your financial plan.

Being mindful of not only your investment costs but also your day-to-day living expenses is essential for establishing a strong foundation for financial success in the future. Take advantage of the NewRetirement Planner today to ensure you’re accounting for all of your expenses as part of your retirement plan.

The post Fees and Expenses on Mutual Funds and ETFs: A Complete Guide to the Often Misunderstood and Hidden Costs of Investments appeared first on NewRetirement.