Tax Season Checklist: 10 Essential Considerations to Review for Your 2023 Return

Tax season is in full swing! You’ve likely either already prepared your tax return or it’s patiently waiting as part of your financial to-do list in the upcoming weeks.

Whether you receive professional assistance or not, getting your taxes in order can be a daunting and difficult task given the many federal and state complexities and often changing rules.

Below we’ll explore 10 key considerations to keep in mind as you review your 2023 tax return prior to sending it off to the IRS.

1. Itemizing or Standard…izing?

A tax deduction is subtracted from your Adjusted Gross Income before taxes are calculated, reducing the amount of taxable income.

Defining a Standard Deduction vs. Itemized Deductions

Each year, you have the option to take one of two main tax deductions:

- Standard Deduction: A fixed dollar amount set by the IRS that can be claimed when you do not have enough qualified expenses to itemize

- In 2023, the standard deduction varied based on your filing status with Single and Married Filing Separately at $13,850, Married Filing Jointly at $27,700 and Head of Household at $20,800

- Individuals 65 or older can claim an additional standard deduction of $1,850 for single or head of household filers and $1,500 for married filing jointly or separately filers, for 2023

- Itemized Deductions: Specific expenses that can be claimed on your tax return, like medical and dental expenses and charitable contributions, among others

Generally, you will take the higher of either the standard deduction or your itemized deductions each year.

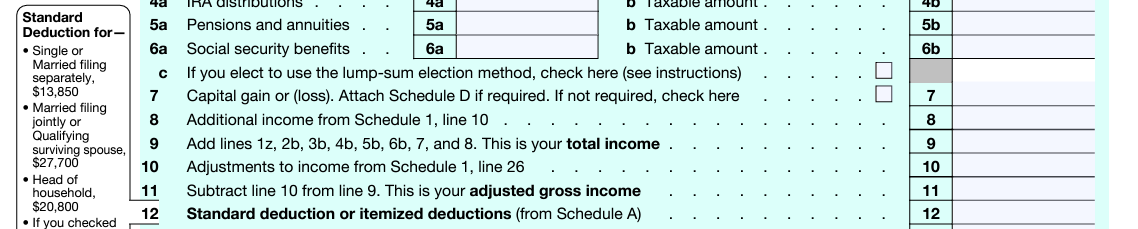

You will find this deduction on the 2023 Form 1040 (The U.S. Individual Income Tax Return), Line 12:

NOTE: The NewRetirement Planner assesses each year whether it’s more beneficial for you to itemize deductions or opt for the standard deduction, considering both the Federal and State levels. Check out Insights > Taxes.

Explore strategies for maximizing your itemized deductions

For future years, if your itemized deductions are close to your standard deduction or even just slightly over, you could consider additional planning to increase your itemized deductions to lower your taxable income even further than the standard deduction.

Bunching is a planning strategy referring to accelerating certain itemized expenses that you planned for the following year into the current year. You may also delay certain expenses for the current year and push them into the following year. The following are some common bunching strategies:

- Charitable contributions: You may consider a Donor Advised Fund to accelerate multiple years’ worth of charitable donations into one year, as the tax benefit is recognized at the time of the contribution into the fund.

- Medical and dental expenses: In 2023, you can deduct qualified, unreimbursed medical and dental expenses that were more than 7.5% of your Adjusted Gross Income. Going forward, consider accelerating or delaying these types of expenses with this threshold in mind.

- Property taxes: If your municipality permits, you may be able to pay a property tax bill assessed in December of the current year in January of the following year and then immediately pay next year’s bill when received in December, essentially bunching the two property tax payments in a single year (Be mindful of the $10,000 cap on deductible state, local and property taxes introduced by the Tax Cuts and Jobs Act in 2017).

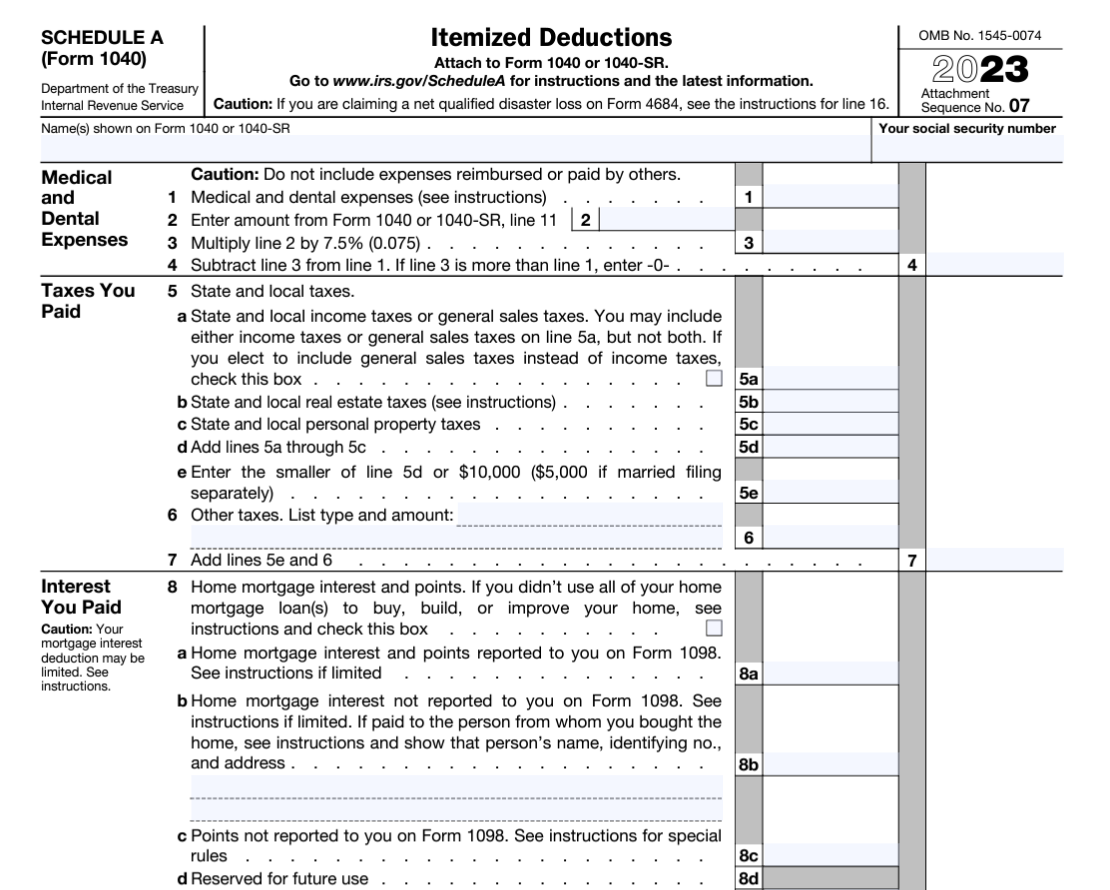

Schedule A (Form 1040) is where you will report Itemized Deductions:

2. Got Dependents? Look Out for These Credits

A dependent that you can claim on your tax return generally refers to either a qualifying child or a qualifying relative. This could include a child, stepchild, sibling or parent.

You will find the dependents section on the first page of your 2023 Form 1040 as shown below:

There are some more common tax credits to be aware of if you have a qualifying dependent. When claiming a tax credit, you are receiving a dollar-for-dollar reduction of your actual tax bill, so they can create some valuable tax savings.

Child tax credit

The 2023 Child Tax Credit is worth up to $2,000 per qualifying child. If your Modified Adjusted Gross Income (MAGI) is over $400,000 (married, filing jointly) or over $200,000 (all other filing statuses), your credit would be reduced by $50 for each $1,000 that your income exceeds the threshold.

There are essentially seven criteria your qualifying dependent has to meet in order to claim the Child Tax Credit:

- Be under 17 years old by the end of the year

- Be claimed as a dependent on your tax return

- Be your child, stepchild, foster child, sibling or a related descendant (like a grandchild, niece, or nephew)

- Rely on you for more than half of their financial support during the year

- Have lived with you over half of the year

- Not file a joint tax return with their spouse unless it’s solely for claiming a refund

- Be a U.S. citizen, national or resident alien

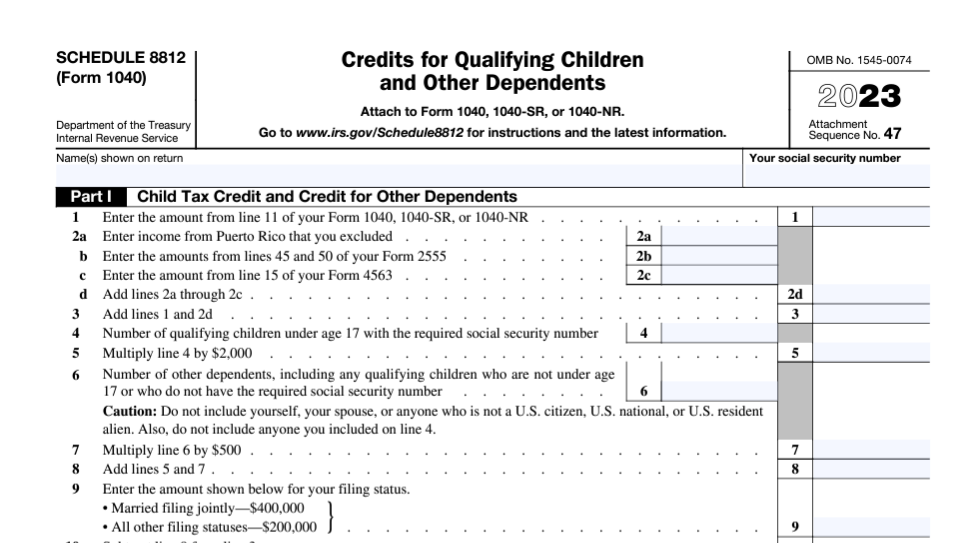

If you pass these tests, go ahead and claim that credit! The credit can be calculated and claimed by filling out Schedule 8812 (Form 1040):

Child and dependent care credit

If you paid expenses for the care of a qualifying dependent to enable you (and your spouse, if married) to work or actively pursue work, you may qualify for the Child and Dependent Care Credit.

In 2023, you can claim up to $3,000 for care expenses if you’re caring for one person, or up to $6,000 for two or more people. The percentage of your qualified expenses that you can claim ranges from 20% to 35%.

The following dependents would be considered qualified and eligible for the credit:

- A child under 13 years old, whom you claim as a dependent on your taxes

- Your spouse, if they’re unable to care for themselves and have lived with you for at least half the year

- Any other claimed dependent on your tax return living with you for at least half the year, who also can’t care for themselves

You (and your spouse, if married) must also have earned income (i.e. work income) to be eligible for the credit. For those with an Adjusted Gross Income (AGI) of $43,000 and above, the maximum credit is $600 for one child and $1,200 for two or more.

In order to determine eligibility and to claim, complete Form 2441:

3. High-Income Earner? Watch Out for the Additional Medicare Tax

No one likes to pay any type of “additional” tax, but it is important to be aware of how you may be impacted by the Additional Medicare Tax of 0.9%.

Most of you are likely familiar with the standard Medicare tax, which is a payroll tax that comes out of your paycheck to help fund the Medicare program. The standard Medicare tax rate is 1.45%, and it’s typically split between the employee and the employer.

The Additional Medicare Tax, or the Medicare Surtax, was introduced as part of the Affordable Care Act and became effective in 2013. It’s an extra tax that applies to certain high-income individuals over a certain threshold. For single tax filers, the threshold is $200,000. If you file your taxes as Married Filing Jointly, the threshold is $250,000.

This tax is on income such as wages, compensation or self-employment income. If you are employed and your income exceeds $200,000 within a calendar year, regardless of filing status or total household income, employers must start deducting 0.9% as Additional Medicare Tax.

You can calculate the Additional Medicare Tax on Form 8959:

4. If the Medicare Surtax Wasn’t Enough, Enter Net Investment Income Tax

Also introduced as part of the Affordable Care Act in 2013 was the Net Investment Income Tax, or NIIT. Essentially, it’s a tax on money made from investments, not from your regular paycheck.

The Net Investment Income Tax applies to individuals who have investment income and meet the same income thresholds discussed above for the Additional Medicare Tax. Some more common types of investment income include:

- Interest, dividends, and capital gains from the sale of stocks, bonds and mutual funds

- Capital gain distributions from mutual funds

- Rental and royalty income

The NIIT rate is 3.8% and it applies to the lesser of:

- Your net investment income OR

- The amount by which your MAGI exceeds the threshold for your filing status

For example, if you file your taxes as single and you earned $250,000 in 2023, and $25,000 of that was net investment income, your NIIT would be calculated on only the income you earned from your investments. This is because $25,000 is less than $50,000, or the difference between the $200,000 cutoff and your $250,000 in income.

Net Investment Income Tax is calculated on Form 8960:

To avoid these additional taxes in the future, it may be worth keeping your income levels below the Medicare and NIIT tax thresholds.

Check your taxable income in the NewRetirement Planner’s Tax Insights.

5. Verify Your Required Minimum Distribution is Satisfied and Reported

Many of you are aware that after reaching a certain age, you are required to spend a portion of your retirement savings throughout your lifetime.

A required minimum distribution (RMD) is the amount of money that must be distributed (or withdrawn) from an employer-sponsored retirement plan funded with pre-tax contributions, such as a 401(k) or a traditional IRA, SEP account, or SIMPLE IRA upon reaching your RMD age.

If you were born:

- Before 01/01/1951, your RMDs have already started

- Between 01/01/1951 and 12/31/1959, then your RMDs must start at age 73

- After 01/01/1960, then your RMDs will begin at age 75

Since RMDs are taxed as ordinary income, just like work income, you’ll need to ensure your RMD is properly reported. If you made a required minimum distribution in 2023, you should have received Form 1099-R. You’ll want to confirm your RMDs were accounted for on the front page of Form 1040 (Lines 4 or 5, depending on the type of account):

Take advantage of the NewRetirement Planner to track an estimate of your anticipated RMDs throughout the lifetime of your plan.

NOTE: There are also various required minimum distribution rules for Inherited IRAs as well. The date of death of the original IRA owner and the type of beneficiary (i.e. spouse, child, etc.) will determine what distribution method to use. These rules can be pretty complex, so you may want to take advantage of this free calculator from Vanguard to gain a better understanding of your Inherited IRA rules.

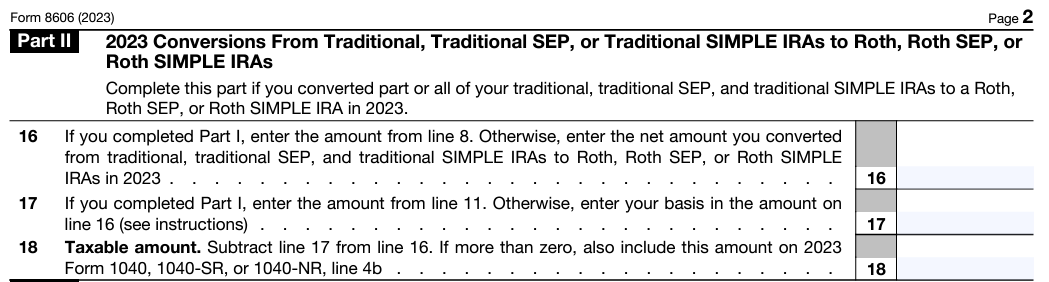

6. You Made a Roth Conversion? Of Course There Are Taxes!

Roth conversions are one of the more popular planning strategies for retirees and, as with most strategies, taxes play an essential role in a conversion.

When you convert from a traditional IRA or 401(k) to a Roth IRA, you will need to pay taxes on the amount that you convert, as it was not previously taxed and it is counted as income.

As you did with the RMD, you should have received Form 1099-R from your custodian (e.g. Fidelity, Vanguard, Schwab) after completing a Roth conversion in 2023. You would then report the Roth conversion on Form 8606, Part II along with your Form 1040:

NOTE: Utilize the Planner to model Roth conversion strategies to determine if you can maximize your estate at longevity, minimize lifetime taxes, or avoid IRMAA fees.

7. Income Too High for a Direct Roth IRA Contribution? Perhaps You Went with the Backdoor Strategy

There are income limits for contributing directly to a Roth IRA. In order to have maxed out a Roth IRA in 2023 ($6,500 if under 50 and $7,500 if 50 or older):

- Single tax filers must have had a MAGI of less than $138,000

- Married filing jointly tax filers must have had a MAGI of less than $218,000

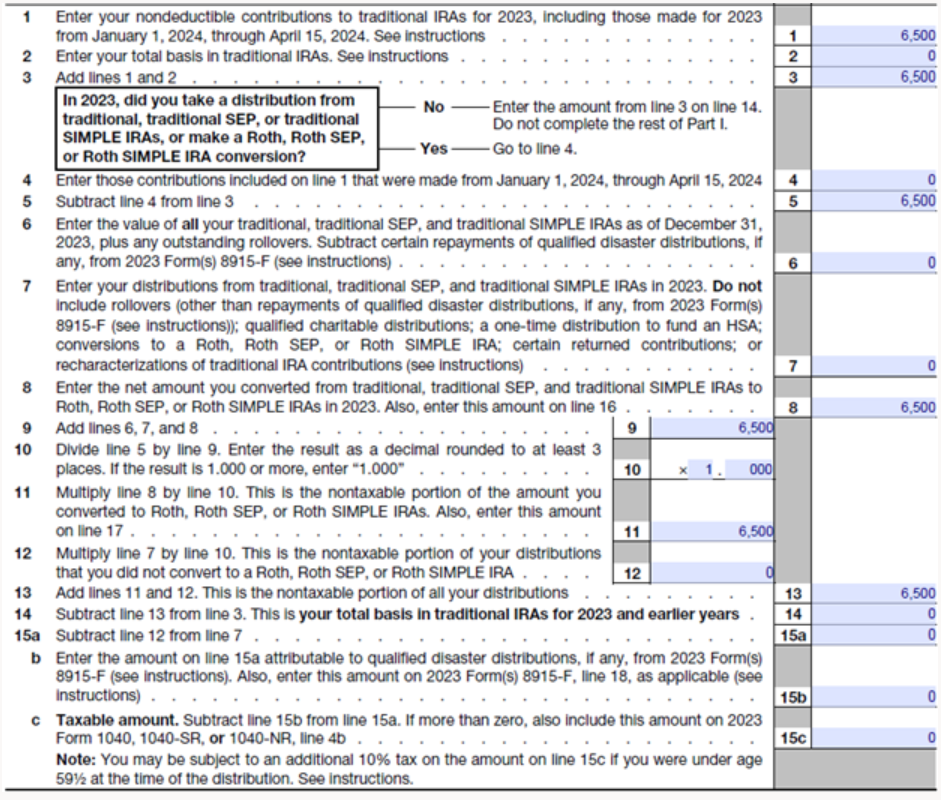

To avoid income limits and still make a contribution into a Roth IRA for 2023, you may have taken advantage of a backdoor Roth IRA contribution strategy. This involves making a non-deductible Traditional IRA contribution and then making a subsequent conversion to a Roth IRA account.

Just like with a Roth conversion, Form 8606 is essential to reporting your backdoor Roth IRA contribution accurately. The non-deductible contribution to the IRA would be reported in Part I of this form. This reflects that you are not taking a tax deduction for the Traditional IRA contribution and preserves the after-tax nature of those dollars, allowing the conversion from the Traditional IRA to the Roth IRA to be a non-taxable event. It may look something like the following:

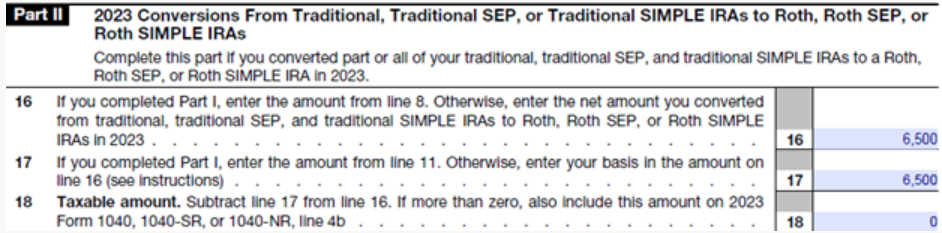

In Part II of Form 8606, you would report the conversion portion and it may look like this:

NOTE: There may be additional complexities to consider, such as conducting a backdoor Roth IRA strategy when you had balances in other IRA accounts, received earnings after making a non-deductible IRA contribution and before converting to a Roth IRA, or spreading the transaction over two years. Consult with a tax professional for further guidance on your specific situation.

8. Retired Last Year? Don’t Forget That Old Retirement Plan

If you retired last year, you may have rolled over your retirement funds from one account to another. For example, you may have rolled over your 401(k) plan with pre-tax dollars to a Traditional IRA.

You’ll want to ensure it was treated as a rollover and not a taxable distribution. You can verify this by, again, looking at the first page of your Form 1040 in 2023. Depending on the type of retirement account, Line 4a or 5a would show the amount of the rollover, while Line 4b or 5b would show $0 as long as no taxable distribution occurred.

If you’re wondering whether you need to report the rollover or transfer of an IRA or retirement plan on your tax return, this IRS calculator will be helpful.

9. Need To Report a QCD?…NBD (No Big Deal)!

If you were at least 70.5 years old or older in 2023 and were feeling charitably inclined, you may have completed a Qualified Charitable Contribution, or QCD.

With a QCD, you are taking a distribution from your IRA and giving it directly to a qualified charitable organization. Given you don’t report QCDs as taxable income, you’ll want to ensure you (or your tax preparer) reported this transaction appropriately.

Like other IRA distributions, QCDs are reported on Line 4 of Form 1040. If part or all of an IRA distribution is a QCD, you’ll see the total amount of the IRA distribution on Line 4a. If the full amount of the distribution is a QCD, you will want to ensure Line 4b is 0. If only part of it is a QCD, the remaining taxable portion will generally be entered on Line 4b. Either way, the IRS wants you to enter “QCD” next to Line 4b.

In the example below, this taxpayer reported a $50,000 IRA distribution, of which $25,000 was a QCD. Since the $25,000 QCD is not taxable, only the remaining $25,000 taxable IRA distribution would be entered in Line 4b.

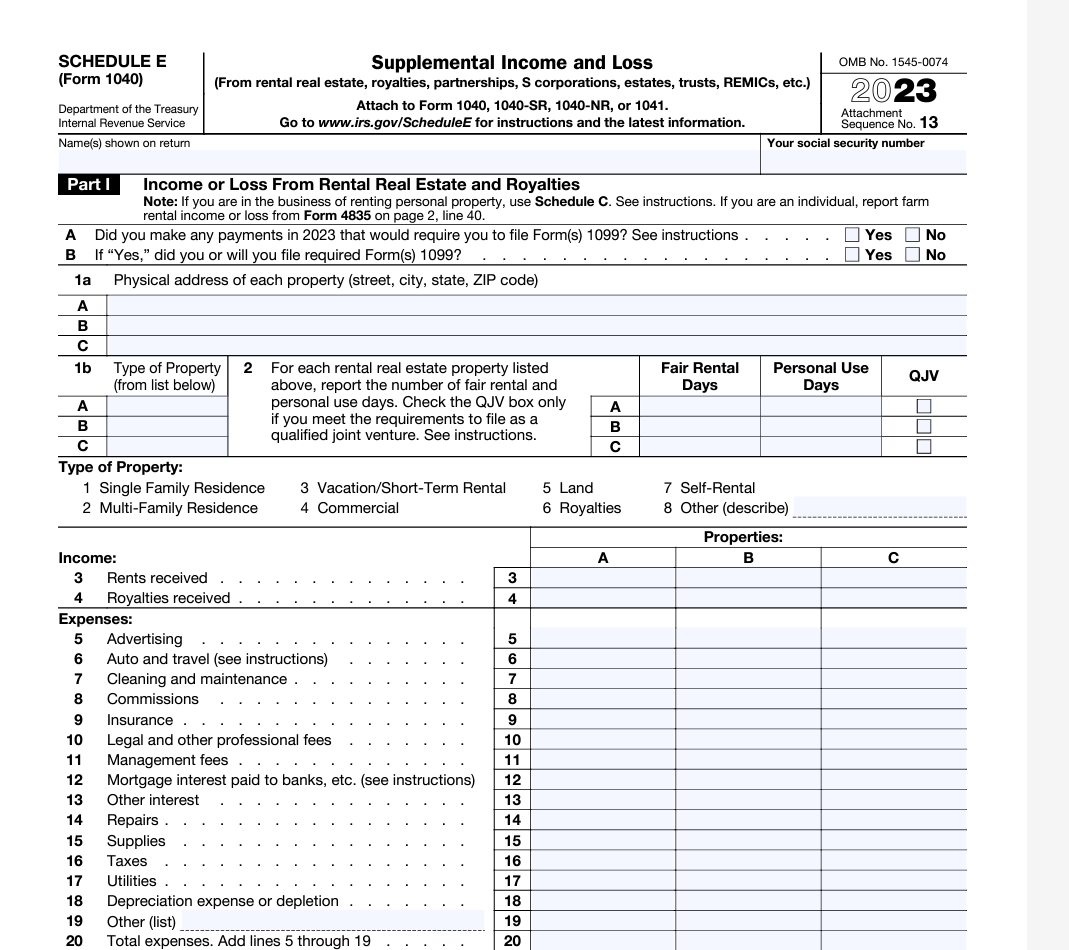

10. Rental Real Estate? There’s a Schedule (E) For That

Rental real estate can be a worthwhile investment, often keeping pace with inflation or even exceeding it. There is a lot of complexity involved with rental properties, especially when it relates to taxes.

For that reason, there is a separate tax schedule dedicated to reporting your rental income and expenses: Schedule E.

As part of your 2023 tax return review, ensure you are reporting your applicable rental income and accounting for all allowable, deductible expenses on the rental property.

Your total rental income (or loss) will flow through to Schedule 1 (1040) and then will land on the front page of your Form 1040, Line 8, as “Additional Income from Schedule 1, line 10”:

NOTE: If you are looking to model your rental real estate property in the NewRetirement Planner, we’ve created this article in our Help Center outlining the steps to take to ensure you are accounting for the various pieces as accurately as possible.

Do a Deep Dive of Your Taxes with the NewRetirement Planner

Taxes are going to continue to play a significant role throughout the lifetime of your financial plan.

The NewRetirement Planner enables you to see your potential tax burden in all future years and get ideas for minimizing this expense. With this tool at your fingertips, tax season may feel a little less stressful going forward.

Want more? Here are additional resources:

25 tax planning tips

Tax talk made simple

Most tax friendly states for retirees

The post Tax Season Checklist: 10 Essential Considerations to Review for Your 2023 Return appeared first on NewRetirement.